Searching for histogram patterns due to macroscopic fluctuations in financial time series

Quelle: http://scholar.sun.ac.za/

Van Zyl, Verena Helen

Datum: 2007-12

Zusammenfassung:

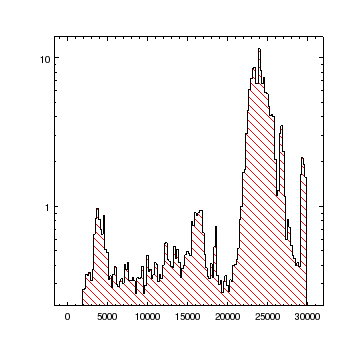

ENGLISH ABSTRACT: his study aims to investigate whether the phenomena found by Shnoll et al. when applying histogram pattern analysis techniques to stochastic processes from chemistry and physics are also present in financial time series, particularly exchange rate and index data. The phenomena are related to fine structure of non-smoothed frequency distributions drawn from statistically insufficient samples of changes and their patterns in time. Shnoll et al. use the notion of macroscopic fluctuations to explain the behaviour of sequences of histograms. Histogram patterns in time adhere to several laws that could not be detected when using time series analysis methods. In this study general approaches are reviewed that may be used to model financial markets and the volatility of price processes in particular. Special emphasis is placed on the modelling of highfrequency data sets and exchange rate data. Following previous studies of the Shnoll phenomena from other fields, different steps of the histogram sequence analysis are carried out to determine whether the findings of Shnoll et al. could also be applied to financial market data. The findings of this thesis widen the understanding of time varying volatility and can aid in financial risk measurement and management. Outcomes of the study include an investigation of time series characteristics in terms of the formation of discrete states, the detection of the near zone effect as proclaimed by Shnoll et al., the periodic recurrence of histogram shapes as well as the synchronous variation in data sets measured in the same time intervals.

Beschreibung:

Thesis (MComm (Business Management))–University of Stellenbosch, 2007.